- Knowing where you’re starting from

- Thinking recovery beyond the company’s borders

- Don’t assume that everything will change or that everything will be as it was before

- Take into account the psychological impacts of containment

- Integrate a new decision-making Framework

We also invite you to share this analysis during a webinar to be held on May 5th from 10 to 11 am.

Chapter 3: Don’t assume that everything will change or that everything will be as it was before

After working on their restart point and taking into account a vision by business chains for the stimulus measures, a more psychological parameter seems essential in the eyes of our customers. It relates to the vision of the future with which the crisis positions us. Is everything going to change? Or on the contrary, will everything return to normal as before?

There are two opposing streams of communication

You have been able to see that for the past few weeks, with a great deal of shocking communications, two extreme currents of communication have been opposing each other.

“Everything will change – nothing will ever be the same again”

Crises are known to create more or less deep, lasting changes in societies, economies and political systems. The current crisis, with its scale and protean impacts, may lead us to think simply that “everything will change”.

The return of economic interventionist welfare states to companies, particularly in Western Europe, will necessarily change the relationship between companies and public actors in a lasting way (see our previous analysis). The desire for the local reindustrialisation of many products (medicines, health equipment, basic necessities, etc.) will be orchestrated by public players and has a direct impact on our economic players. Some analysts believe they see it as a complete modification of our capitalist system and the role that our companies play in it. It is true that the social utility of each company is already being questioned. Companies that are unable to produce anything useful to society on their own at present will not emerge as winners.

The individual behaviour of our societies is already undergoing changes linked to the crisis. The health risks linked to contacts between individuals will change our relationships with places where we live together, as varied as restaurants, bars, public transport, open spaces, theatres, stadiums, etc. When these behaviours are coupled with changes that are already in the air, such as the “shame of flying”, particularly among the new generations, they have an even greater impact: will we travel as much as before and in the same way after this crisis?

” It’s just a reboot”

One of the recognized virtues of a crisis, often well after the fact, is to foster a new impetus for companies emerging from it. As if nothing had happened?

Consumer capitalism seems to regain its rights as soon as the doors of business and consumers are reopened. For example, the Hermès store in Guangzhou, China, posted record sales on the very day it reopened after the lockdown, for a total of 2.7 million euros! Similarly, in France, the reopening of McDonalds, a company that is symbolic of global capitalism, created unprecedented traffic jams, as in Moissy in Seine-et-Marne. When the economy picks up again, consumption peaks are to be expected and records will be broken. The forced under-consumption and the catching-up of consumers to make up for their shortfalls, coupled with the current caution of companies in BtoB consumption in the context of uncertainty about the future, are logical peaks. But are these peaks the prelude to “just a restart” of consumer capitalism or are they just cyclical and will be quickly erased by the new consumer awareness fomented by the period of confinement (why do I need to consume so much, and what if I travelled more often in my own country…)?

If consumption starts up again and companies start to catch up with aggressive production, what about the unprecedented reduction in CO2 emissions due to the enormous reduction in industrial activities and transport? Would it also only be a meagre temporary ecological respite for the planet?

On the subject of the companies that will disappear, precipitated into bankruptcy despite government support, the proponents of “just a restart” argue that this is merely a somewhat forced “creative destruction”. A “creative destruction” not driven by innovation but by the impact of the crisis on certain areas of activity. Other companies will naturally recreate themselves, that’s all.

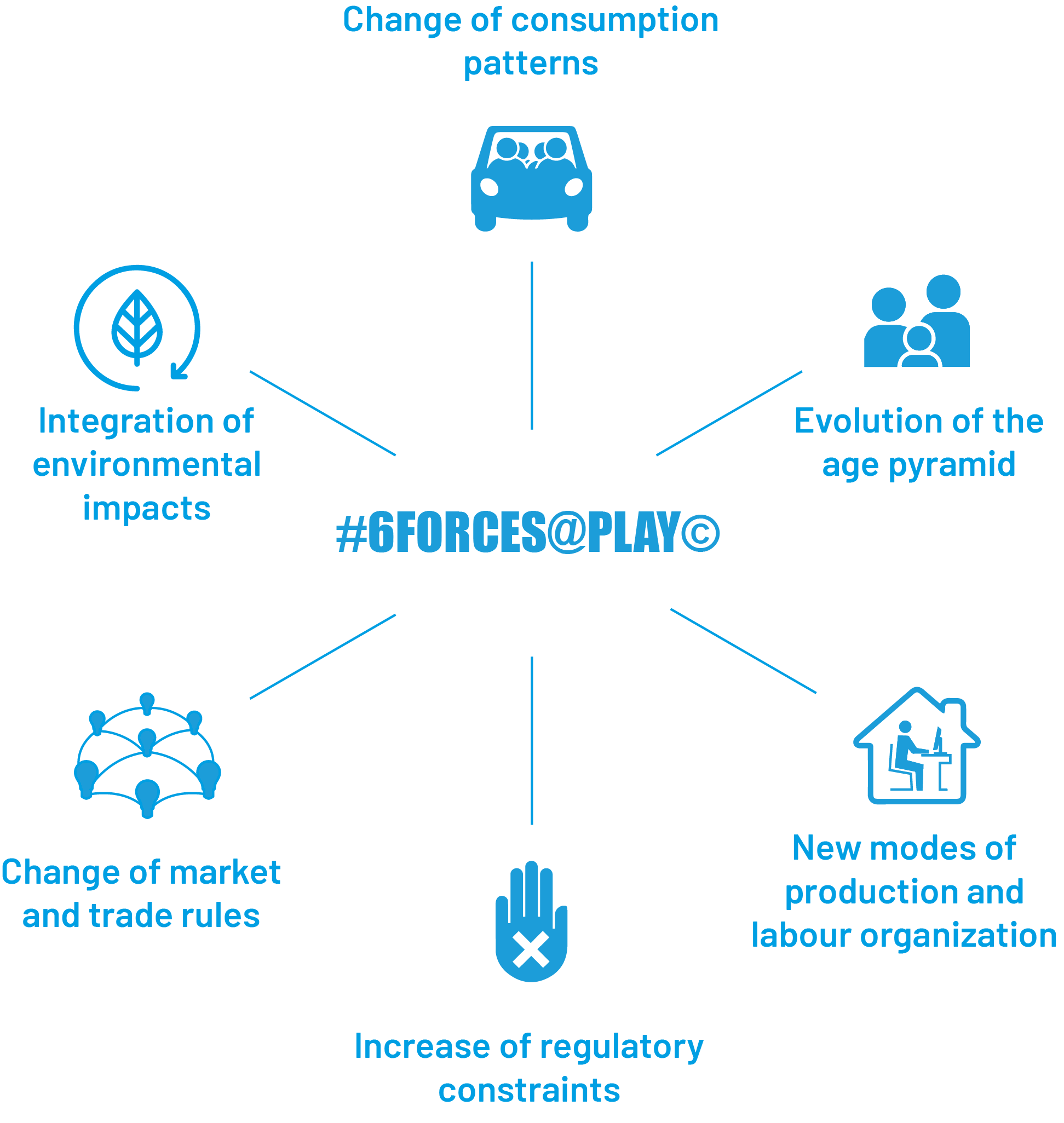

6 restart trend readings

Bengs has developed the 6 forces analysis grid with the help of managers from large companies mobilized in the Bengs Lab, our Open Innovation laboratory analyzing market disruptions and working collectively on the creation of innovative business models.

This 6 forces analysis grid allows us to think about these two extremes and to draw the contours of the restarting world.

Change of consumption patterns

Both the increase in online sales promoted by maintaining and supporting delivery activities (on this subject, see the e-commerce curves provided by CCInsight), and the examples of the consumption boom in reopened stores (Hermès, McDonalds…), may herald a return to traditional consumption patterns in a certain continuity. The share of e-commerce would certainly increase, but it had already been structurally on the rise for several years.

But from the other point of view, the prospects of a sharp drop in countries’ GDPs and an economic recession that is difficult to recover, as well as the impact of other factors on consumption (health restrictions in shops, for example) encourage us not to adopt the discourse that everything will be as it was before from a consumption point of view.

Beyond the somewhat misleading magnifying glass effects on current consumption indicators, both the volume of consumption and the way of consuming will change when the recovery takes hold.

Evolution of the age pyramid

The impact of this parameter relative to the others has never been stronger on the current crisis analysis. Firstly, government decisions and recommendations on individual freedoms are linked to different age groups. On the one hand, the youngest populations are gradually returning to school in France from 11 May onwards, in a progressiveness directly linked to the age of the schoolchildren. On the other hand, the seniors, to whom it was recommended to remain confined for a long time. The problems of social isolation, consumption patterns and home services for seniors, which companies have been dealing with more and more in recent years in order to meet growing needs (the famous “silver economy”), are both highlighted by the situation and call for new solutions. For example, a reflection between two opposing models of organization and development of territories to take care of seniors is necessary: should we encourage a kind of ghettoization of seniors in medical buildings grouping all services to support them, or rather promote intergenerational houses whose lower floors would be reserved for the oldest, upper floors for student studios, intermediate floors for families and a medical-social staff shared between early childhood and the most senior?

The crisis situation of elderly dependent people housing structures (EHPAD), and in particular the lack of means to support our seniors at the end of their lives, challenges, shocks and calls for strong social choices, at a time when the ageing of populations is upsetting the balance (23.8% of over 60 year olds in France in 2013 against 29.6% in 2030, and 32.9% in 2050 according to INSEE projections). From the point of view of the generational pyramid, the crisis has a real impact on taking into account the differentiated needs of generations and the constraints of individual freedoms and opens up new reflections on intergenerational living together.

New modes of production and labour organization

Accessibility constraints in the workplace will be sustainable until the crisis is gradually overcome, as shown by the latest announcements by French Prime Minister Edouard Philippe on 28 April 2020.

The integration of constraints in the conditions of access to one’s physical workplace, both in terms of home-workplace travel and the internal organisation of the workplace have a strong impact on this angle of analysis.

This third force is going to undergo a radical change due to the fact that the unity of place and company time is disappearing as a result of the crisis. The very organization of work is being modified in all aspects: Social law is being revised, the right to leave is being reviewed for economic reasons, working hours will be modified to limit transport congestion, compensatory rest periods will be adapted, management models will evolve to integrate massive distance working, and the corporate culture and employee attachment will be disrupted, and finally, the location of employees in relation to the physical location of the company will change paradigms… Even if certain professions will experience a more traditional revival because they have a real need to go to the physical workplace (construction and public works, production plants, transport operators, etc.), the main change will be an adaptation to health constraints, the overall organisation of work will undergo major changes.

These changes will not be temporary because, firstly, the deconfinement plans will be progressive, secondly, scientists are encouraging people to plan to live with the virus for at least another 12 months even if the situation stabilises before then, and thirdly, because structurally the increase in the world population and flows will encourage the future appearance of other health crises which countries will want to be able to deal with more effectively.

It is thus certain that from the point of view of this strength of the “New modes of production and work organisation”, it is not just a question of a simple restart and that the changes will be strong and lasting.

Increase of regulatory constraints

Containment has opened up a field of possible regulatory opportunities that is both rapid and unprecedented. To meet the new needs of confined populations, States have adopted regulatory measures on subjects as varied as teleconsultation, home delivery of medicines, labour law, public-private financing rules, and the public procurement code to make the public procurement process more flexible, State intervention in private activities, the investment ratio of companies via state-guaranteed loans… New measures that sometimes run counter to the principles of social dumping as laid down by European Union and OECD rules.

During the recovery, it is to be expected that some temporary regulations will be abandoned at the end of the crisis, but also that others will be kept for longer, adapted to long-term application and to be voted as laws.

Our French companies that have lived in a model of very high labour costs compared to world averages are discovering a model where the French government is setting up a programme to protect the salaries of the most secure and best endowed on the planet via the massive short-time working scheme that transfers this wage cost to the public sector. The French regulatory balance is being revisited and tomorrow’s regulations on both social (medical teleconsultation) and economic issues (support for independent entrepreneurs) will evolve over the long term in a way that is still difficult to predict.

Change of market and trade rules

Highlighting the strong interweaving between the business chains raises questions about the global supply chain that has been gradually built up since the 1970s and which has made China the world’s production plant. Western countries are turning to reindustrialization programs in nearby geographic hubs. However, the adaptation of market and trade rules to the massive reindustrialisation of countries with highly service driven economies raises many questions. For example, the reindustrialization of drug production in France mechanically generates an increase in unit production costs and therefore requires an adaptation of the Social Security reimbursement scales. Who will bear the costs? How can the rules of the market and of exchange between the private economy and the public authorities be adapted to bear the costs of relocations by limiting the carry-over on consumer purchase prices?

Market rules will also evolve according to the political choices of investment priorities in certain sectors, favouring some to the detriment of others because financing capacities are limited.

Integration of environmental impacts

As we have seen, the consumption patterns of certain services and products are evolving in a positive direction for CO2 emissions (reduction of industrial pollution, air transport-related pollution, etc.) and the upturn raises the question of the sustainability of these impacts. More generally, the management of economic decline will be linked to the integration of environmental impacts. It will take several decades to wipe the slate clean from the survival and recovery plans of public authorities. Is this an opportunity to integrate the notion of environmental impacts into the recovery?

This is a complex issue for many industries. Western countries have got into the habit of exporting a lot of polluting waste to be treated elsewhere, where reprocessing costs are lower but environmental standards are less stringent. But if we want to relocate plastics reprocessing to regain industrial independence and limit the flow of goods when restarting, how can we manage the cost? How to arbitrate between the economic and environmental issues?

By integrating these 6 forces in our analysis of the recovery, we ask the question of giving a more sustainable direction to the economic recovery

Don’t assume that everything is going to change. Not considering that everything will be as it was before

Uncertainty about the future and the resulting anxiety can disturb the business leader and lead him or her to simplify the reasoning. If everything is going to change, you can start from scratch by completely redesigning your company! If nothing is going to change, you wisely wait for the storm to pass before resuming your activity as if nothing had happened. In both cases, your strategic roadmap will be wrong because it will not take into account past behaviors that will resume as they are, those that will evolve slightly for a longer or shorter period of time, and those that will radically and durably change.

Our world does not know the end of something or the restart of an identical one. It is indeed an evolution, a multi-dimensional evolution guided by a new course. However, the duration of this evolution to reach the target of this new course is likely to be very long. The deconfinement plan announced by Mr. Edouard Philippe today clearly shows that before any evolution, we are going through a transition period of varying length depending on factors that are not all within our control. The change in the political, economic and social system is going to be a long one. But our new start is a good starting point for a new future.

In order to anticipate this new future, our clients’ managers are asking us the following question: what individual and collective behaviours will be merely cyclical, and which ones will durably modify my organisation, my business model, my regulatory constraints, my environmental impact, the needs of consumers and my clients? To what extent will I have to pivot and innovate in my product and/or service offering to take into account sustainable changes?

Follow our news and join us on 5 May 2020 from 10 to 11 am for a webinar dedicated to this topic!